I

t would be difficult to find someone more cautious

than Harvey Wood, a third generation Arizona cotton and

citrus farmer. In more than 30 years of farming, he never

had an accident.

Harvey was cautious about his financial affairs too. Shortly

after marrying his high school sweetheart, Sandy, he bought

life insurance to make sure she’d always be protected. Over

time, Harvey realized that his coverage hadn’t kept up with

growing needs. He and Sandy now had young children and the

farm was expanding. That’s when Harvey met with insurance

agents, Bryan Buzzard and Bob Sapanaro. After their

comprehensive financial needs analysis, he took their

advice and significantly increased his coverage.

Still, there were years when crops were ruined

and Harvey didn’t know how he could afford the

premiums. Knowing how much Harvey needed the

coverage, his agents discussed with him how to use

the cash values in his whole life policy to keep the

insurance in force.

1

Several years later, Harvey, 50, was refilling a

fertilizer tank in front of a tractor when it slipped

into gear and killed him. Sandy and the kids were

devastated, but there was hardly time to grieve.

They quickly realized that the world wouldn’t stop

simply because tragedy had struck. The crops and

the bills kept growing. “We owed hundreds of thou-

sands of dollars," says Sandy. “I kept thinking, ‘this

farm has been in our family for generations, I can’t

lose it now.’"

But that’s why Harvey had purchased and kept

the additional life insurance. With it Sandy paid off

the farm debt, college loans, the mortgage and credit card

bills. Today, the family is thriving. Sandy handles the

business side of the farm, while her son, H.C., manages the

farming operations.

“Our life is forever different without Harvey," says

Sandy, “but because he cared so much and bought the life

insurance, our way of life hasn’t changed."

1

Borrowing against a policy’s cash value to pay premiums will reduce the cash

value and death benefit, but can keep a policy in force in difficult times.

Planning Rescues a Farm

Insuring Your Most Valuable Farm Asset . . . You!

The Life and Health Insurance Foundation for Education is a nonprofit organization dedicated to helping consumers make smart

insurance decisions to safeguard their families’ financial futures. © 2007 LIFE. All rights reserved.

®

T

he most important asset on any family farm is not the equipment

or the livestock or even the land. It's the farmer. Would your

family business survive if something were to happen to you.

Smar t insurance planning can help ensure that it will.

.

Life insurance proceeds can pay off your far m's debts, giving

your survivors precious time to decide how to move forward. If

they sell the far m, they'll have the freedom to seek the best

price rather than settle for less in a distressed sale.

.

Disability insurance provides replacement income if you

become injured or sick and are unable to work the far m for

a period of time.

.

A buy-sell agreement allows surviving par tners to buy out

your share of the business at a fair price using life or disability

insurance proceeds.

.

Key person insurance provides the farm owner with the financial

flexibility to hire a replacement when a key employee dies.

www.life-line.org

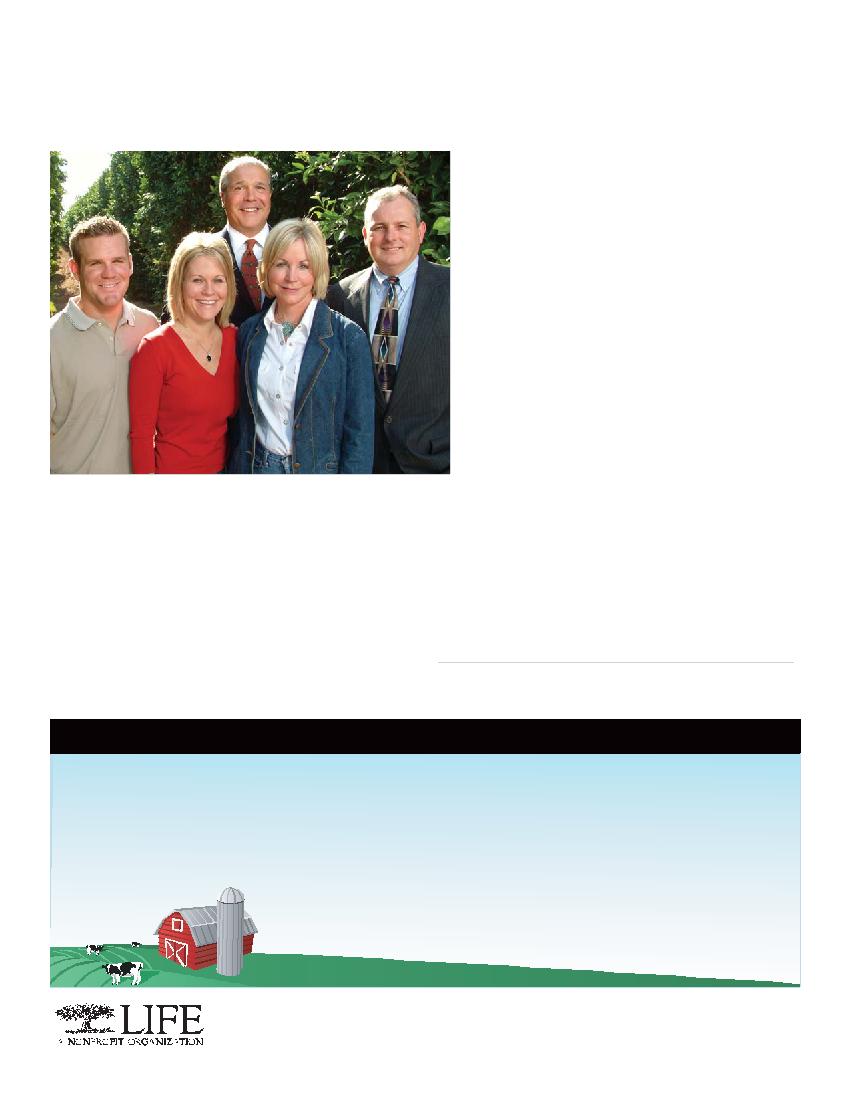

Agents Bob Sapanaro (center) and Bryan Buzzard (far right), with client

Sandy Wood (second from right) and her children